The 20% Rule

The neon-green sneakers in the shop window were practically screaming Aisha’s name. They were bold, stylish, and exactly what she needed to complete her outfit for her friend’s birthday party next month.

She pulled out her phone to check her balance. Her monthly allowance and the small stipend from her weekend gig helping an aunt with graphic design had just hit her account: ₦50,000. The sneakers cost ₦45,000.

“If I buy them, I’ll have ₦5,000 left for the whole month,” Aisha muttered to herself, her thumb hovering over the “buy” button on the store’s website. “I can survive on instant noodles, right?”

“Bad idea,” a voice chimed in. It was her older brother, Tariq, leaning over her shoulder. “You said the same thing last month about that jacket, and by week two, you were borrowing money from me for bus fare.”

Aisha sighed, locking her phone. “I want to save, Tariq. I really do. I want to buy a proper digital drawing tablet by the end of the year. But every time money hits my account, it just… evaporates. I don’t know how people build a habit out of this. It feels like torture.”

Tariq smiled, sitting down across from her. “That’s because you’re trying to save what’s left after spending. You have to flip the script. You need a system that doesn’t rely on willpower, because willpower fails when neon sneakers are involved.”

He grabbed a piece of paper and a pen. “Let’s build the habit using three simple rules.”

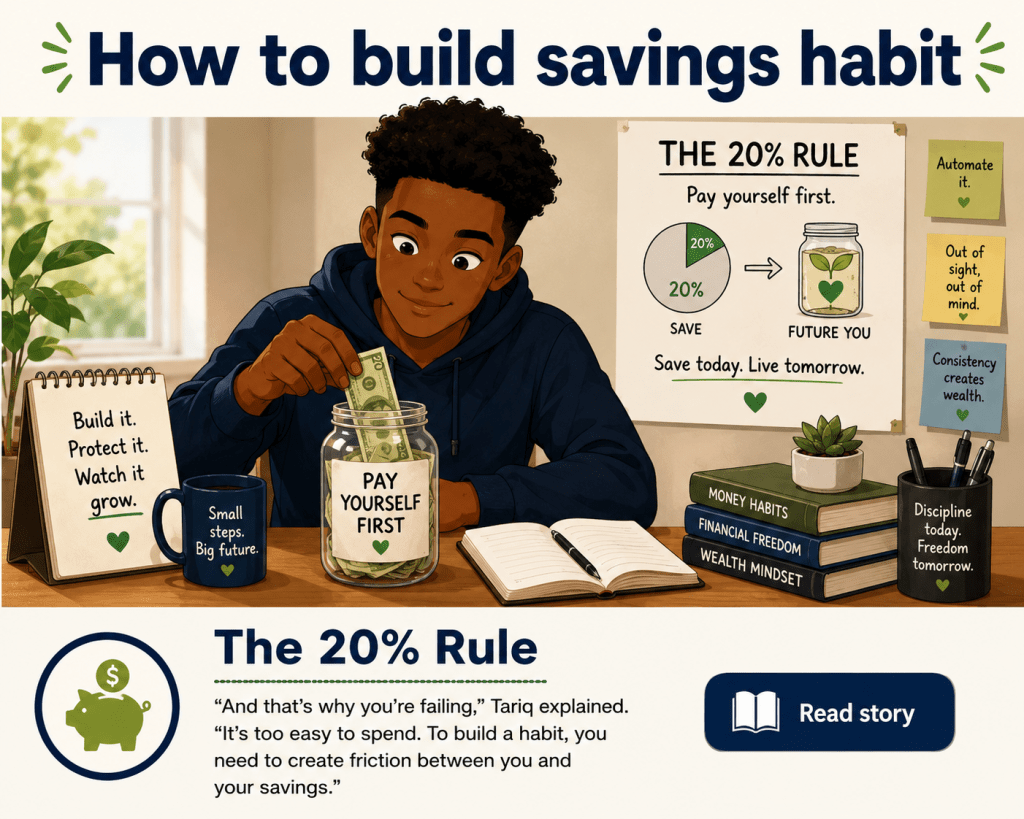

Step 1: Pay Yourself First (The 20% Rule)

“Right now, you treat saving like an afterthought,” Tariq said, drawing a circle and slicing off a small piece. “From now on, the moment money touches your hand, 20% goes straight to savings. No thinking, no debating. For your ₦50,000, that’s ₦10,000. You move it immediately.”

“But then I only have ₦40,000 left to spend,” Aisha countered.

“Exactly. You force yourself to live on the 80%. It’s much easier to budget when the temptation is entirely out of sight.”

Step 2: Build a Friction Barrier

“Where do you keep your money?” Tariq asked.

“Just in my main bank account. It’s linked to my debit card and my phone’s fast-pay app.”

“And that’s why you’re failing,” Tariq explained. “It’s too easy to spend. To build a habit, you need to create friction between you and your savings. Open a separate high-yield savings account or use a digital piggy-bank app. Move that 20% there. Do not link a card to it, and do not keep the app on your phone’s home screen. Make it a hassle to take the money out.”

Step 3: Use the 48-Hour Rule

Aisha pointed at the screen. “Okay, but what about the sneakers? I still want them.”

“If you still want them in 48 hours, we can look at your 80% spending budget and see if you can afford them over two months,” Tariq said. “Most impulse buys are just a temporary rush. If you force yourself to wait two days before hitting buy, the urge usually fades.”

Aisha looked at the paper, then at her phone. It sounded mechanical, but she was tired of being broke by the middle of the month.

She opened her banking app. Before she could talk herself out of it, she transferred ₦10,000 into a locked savings wallet she had opened months ago but never used. She then deleted the retail app from her home screen.

The first week was tough. Aisha had to say no to a couple of expensive fast-food hangouts with friends, opting to eat at home before going out instead. But a strange thing happened: because her main account balance was lower, she naturally became more protective of it. She started tracking where her cash went.

By the end of the month, a miracle occurred. Aisha checked her main account—she had ₦2,000 left. But when she checked her hidden savings wallet, there was a crisp, untouched ₦10,000 sitting there.

She hadn’t starved. She hadn’t missed out on life. She had just automated her discipline.

When her next payment arrived, Aisha didn’t even hesitate. She immediately moved 20% into her savings. The habit had officially taken root, and for the first time, that digital drawing tablet felt less like a distant dream and more like a guaranteed reality.

Leave a comment