The glow of his laptop screen was the only light in Segun’s apartment as the clock struck midnight.

On the screen was his bank statement, and the numbers didn’t make sense.

Segun was a brilliant junior structural engineer. He spent his days calculating load distributions for massive multi-story buildings, managing complex stress tolerances down to the millimeter. Yet, looking at his personal finances, he felt like he was standing under a collapsing roof.

He had received his salary exactly twelve days ago. Now, looking at his balance, more than 70% of it was completely gone.

”Where did it go?” he muttered, rubbing his temples. He hadn’t bought a new phone, he hadn’t traveled, and he hadn’t made any major purchases. His money hadn’t vanished in a massive wave; it had slowly bled out through a hundred invisible cuts.

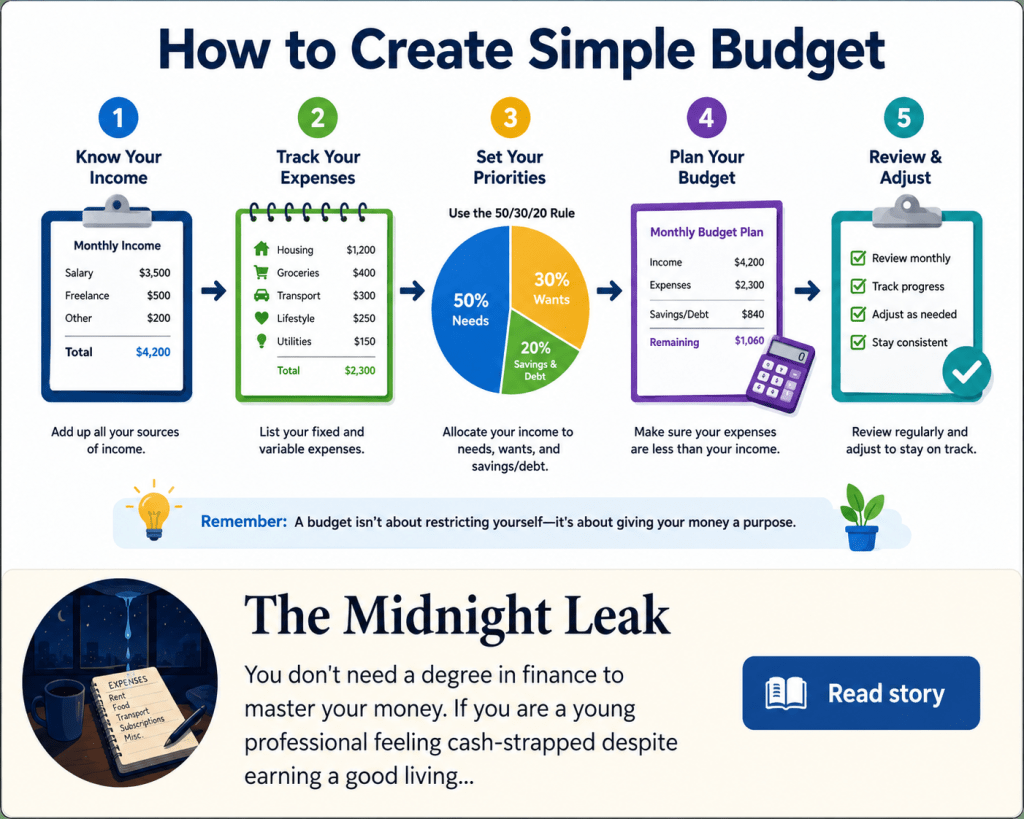

Frustrated, Segun opened a blank spreadsheet. He was determined to treat his money the same way he treated an engineering project: by running a diagnostic audit. He didn’t use a complicated, expensive financial tracking app. Instead, he decided to use the simplest structural framework in finance—the 50/30/20 Blueprint.

First, he looked at his Needs (50%). He wrote down his non-negotiable survival costs: rent, utilities, basic groceries, and his daily commute. When he totaled them up, he realized they were perfectly fine. The foundation of his building was solid.

Next, he looked at his Savings & Debt (20%). He stared at the empty row. For the past six months, this number had been a flat zero. He was saving whatever was “left over” at the end of the month, which always turned out to be nothing.

Finally, he looked at the danger zone: his Wants (30%). This was where the hidden leak lay.

As Segun cross-referenced his bank statement, the culprits stepped into the light. It wasn’t the occasional weekend dinner with friends that broke him; it was the automatic, unmonitored daily friction costs. The mid-day gourmet coffee deliveries at the office, three different streaming subscriptions he rarely watched, and the impulsive “one-click” online shopping orders late at night. Individually, they were small numbers. Together, they were a financial flash flood.

Right then, Segun rewrote the logic of his finances. He didn’t vow to live like a monk or stop enjoying his life. Instead, he gave every single currency unit a job before the month started.

He set up an automatic transfer that moved 20% of his salary into a separate investment account the exact morning his paycheck arrived—making his savings completely invisible and untouchable. He allocated 50% strictly to his bills. The remaining 30% went into a separate digital wallet. That was his guilt-free spending money. If that wallet hit zero on day fifteen, the fun stopped until the next month. No exceptions.

Four weeks later, midnight came around again. Segun sat at his desk, but the suffocating anxiety was gone. His laptop screen showed his savings account sitting exactly where it belonged, growing quietly in the background.

He smiled, closing the spreadsheet. He had finally plugged the leak.

Leave a comment